By Michael Green and David Berns, PhD, CIO & Cofounder of Simplify ETFs.

Introduction

The extraordinary credit crisis that emerged in the mortgage market in 2007-2008 introduced the investment world to the concept of credit hedging and the potential for asymmetric returns in financial products like Credit Default Swaps (CDS). Unfortunately, enthusiasm for these trades, regulatory changes, and policy responses changed the available payoff profiles in credit hedges. As a result, investors have been relentlessly disappointed with credit hedging techniques, even as the return potential in credit has declined with tight credit spreads and low risk-free yields.

The high cost and disappointing performance of credit hedging leave investors with a quandary – how, if at all, can credit risk be hedged efficiently? This blog shows how a long-short exposure to the quality-junk factor (Q-J) can potentially function as an efficient credit hedge within a costly hedging space.

Theory Behind Credit Hedging with the Quality-Junk Factor

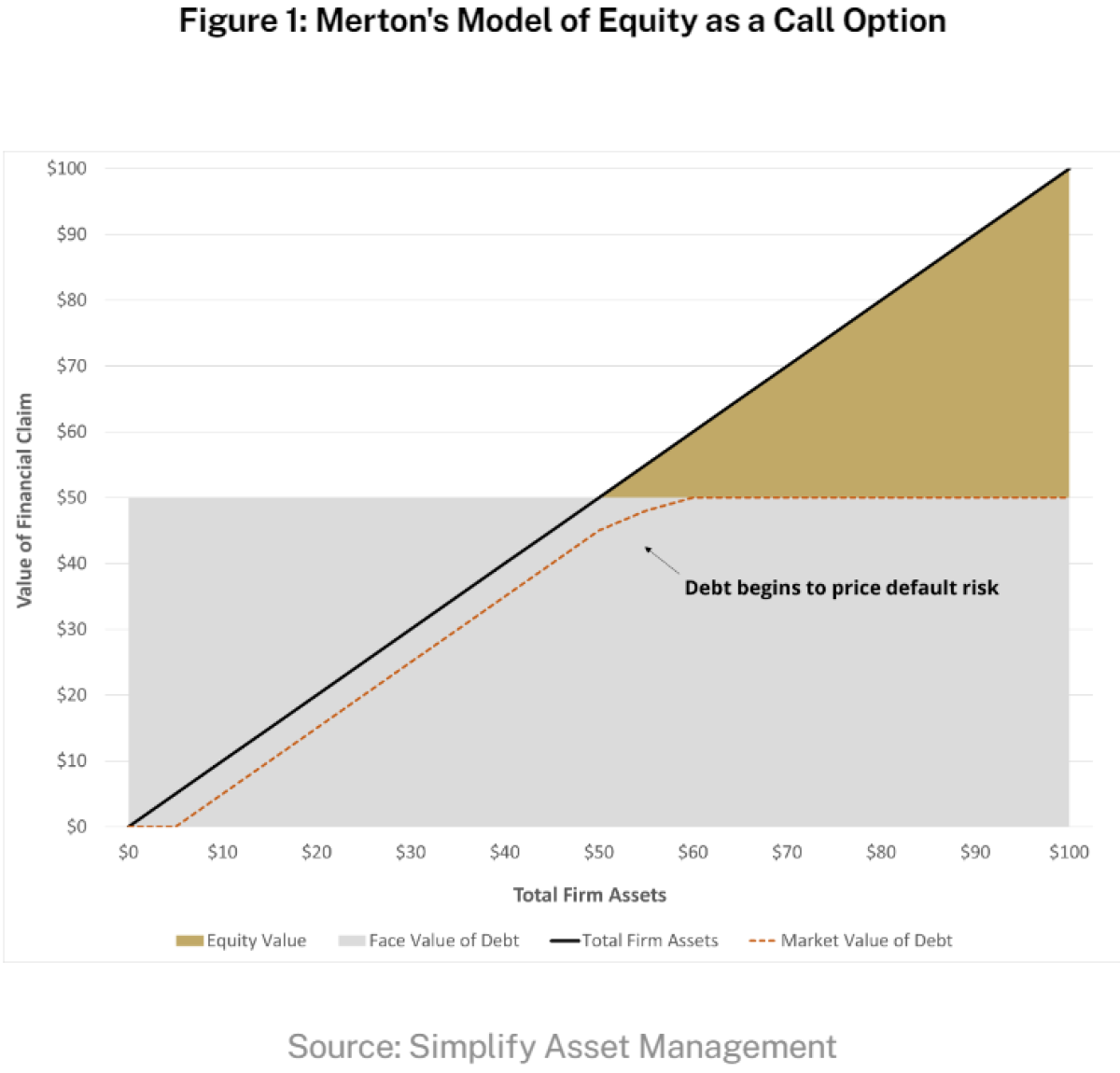

In 1974, Robert Merton introduced the “Merton Model” of credit and equity as competing claims on underlying asset value. In this model, equity can be thought of as a call option on the value of total firm assets above the notional (face value) level of debt, as depicted in Figure 1.

As many academics and practitioners have noted, this relationship introduces the potential to model credit exposures and credit hedges as options as well. For example, the creation of Credit Default Swaps (CDS), made famous in Michael Lewis' book, The Big Short, relied on these insights to create the equivalent of a call option on credit default risk.

The Merton model naturally leads to an alternative to using CDS to obtain credit hedging properties – an equity long/short expression that pairs a long in high-quality, low-leverage equities with a short in low-quality, high-leverage equities. The quality equities are essentially deep-in-the-money calls (on asset value), while the junk equities are at-the-money calls, creating an asymmetric response from the long/short portfolio when a risk-off event occurs and asset values drop below debt face values for the junk names.

Let's now take a look at this empirically

The Quality-Junk Factor in Practice

We create our quality basket by screening for the highest decile of names by margins, profit stability, and balance sheet strength from the 1000 most liquid stocks and enforcing equal-weight sector exposures. We then create a junk basket from the same 1000 names, again with sector limits, screening for the highest decile of sensitivity to an increase in debt refinancing costs. These legs don’t mirror each other from a characteristics perspective on purpose; we do not want to overweight a single factor causing excessive volatility in the hedge. Our Q-J portfolio is then 100% long Q and 70% short J, to stay near beta-neutral. This configuration is also relatively sector-neutral, helping avoid unintended basis risk through extreme allocations to any given sector.

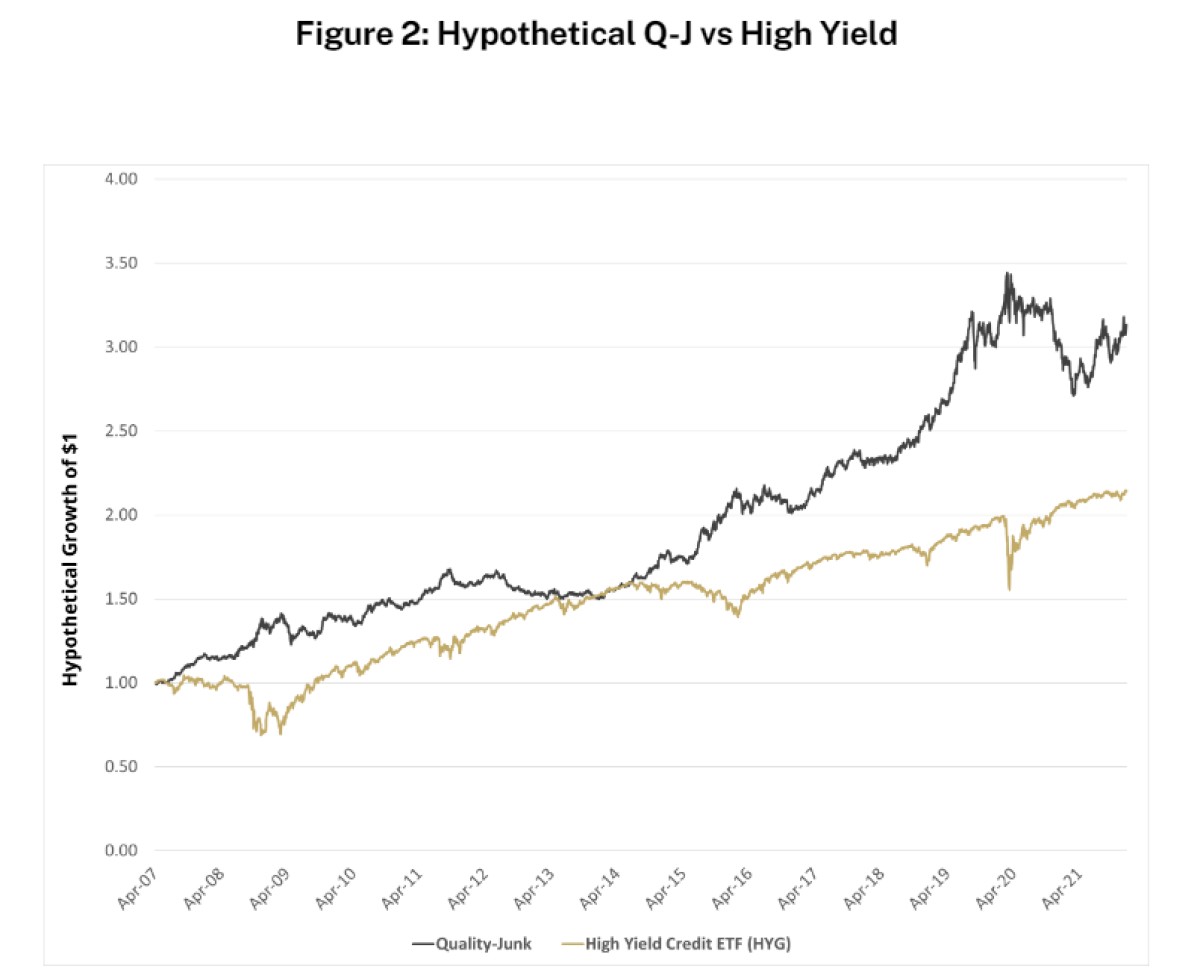

From the lens of the above screening criteria, the prediction that Q-J should act as a credit hedge seems intact: the long Q position has low sensitivity to financing costs (credit spreads) while the short J has a high sensitivity to widening credit spreads. In Figure 2, we show hypothetical performance for this definition of Q-J compared to high-yield markets using a backtest. As expected, we see strong outperformance during risk-off periods, precisely acting like a credit hedge. In addition, we also see a very positive carry outside of the risk-off events, an incredibly beneficial feature for a credit hedge in low-yield environments.

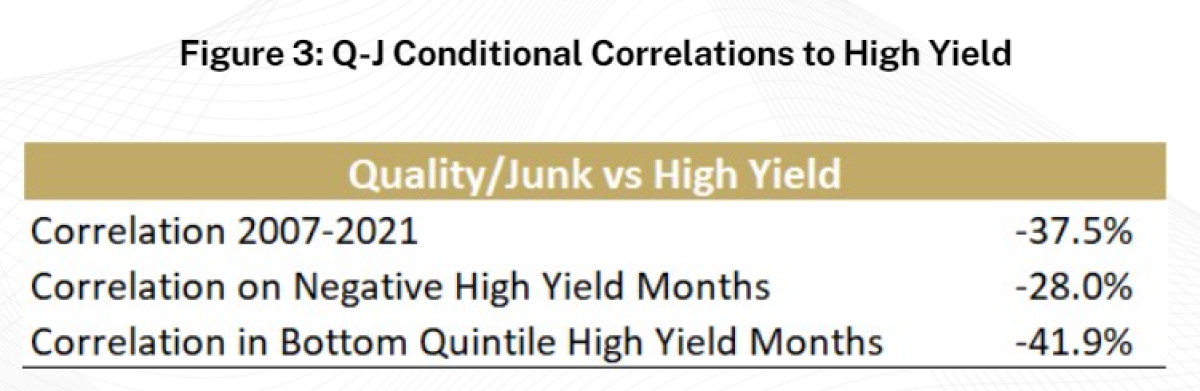

Figure 3 takes another look at the credit hedging properties of Q-J. Again, we see that the correlation to high yield is consistently negative in the worst-performing months for high-yield credit, even while the absolute return from the hedge is positive – again, a critical consideration in an environment of low absolute returns.

Conclusion

In an environment characterized by low absolute yields and high levels of corporate credit risk, efficient credit hedging becomes much more critical in portfolio construction. Fortunately, we believe this is possible. A thoughtfully constructed overlay of quality vs. junk equity in a long/short implementation potentially offers a combination of positive carry with negative correlation to credit, creating the potential for improved returns at lower risk.

About the Author:

Michael Green, CFA, has been a student of markets and market structure, for nearly 30 years. His proprietary research into the shift from actively managed portfolios and investment funds to systematic passive investment strategies has been presented to the Federal Reserve, the BIS, the IMF and numerous other industry groups and associations.

Michael joined Simplify in April 2021 after serving as Chief Strategist and Portfolio Manager for Logica Capital Advisers, LLC. Prior to Logica, Michael managed macro strategies at Thiel Macro, LLC, an investment firm that manages the personal capital of Peter Thiel. Prior to Thiel, Michael founded Ice Farm Capital, a discretionary global macro hedge fund seeded by Soros Fund Management. From 2006-2014, Michael founded and managed the New York office of Canyon Capital Advisors, a $23B multi-strategy hedge fund based in Los Angeles, CA, where he established their global macro strategies, managing in excess of $5B of exposure across equity, credit, FX, commodity and derivative markets.

In addition to his work as a market theorist and portfolio manager, Michael has been noted for his work as a public speaker and financial media participant. He is a graduate of the Wharton School at the University of Pennsylvania and a CFA holder.